UHNW Institute

Achieving Best-In-Class Wealth Management Integration

How should wealth advisors work together to ensure that they deliver the best possible service to UHNW families, particularly given their often complex needs? This article from the UHNW Institute in the US sets out some guidelines.

The following article comes from the UHNW Institute, the US-based think tank with which FWR is the exclusive media partner. This article examines the ways that families get the most out of their advisors in handling their complex business and non-business affairs. It sets out some pointers and illustrates the landscape that advisors and families must navigate. The author is Joe Calabrese, who is a member of the institute's advisory board, and National Head of Wealth Advisory Services at Key Private Bank.

The editors of this news service are pleased to share these insights. Further examples of UHNW Institute commentary and analysis can be found by clicking on the “categories” button on this news service and going to the UHNW Institute field. (See here for a list of content.)

For an ultra-high net worth (UHNW) family’s strategy to succeed, it is accepted wisdom that the efforts of its advisory team members must be integrated. However, being widely accepted doesn’t mean integration is easy to do. In fact, effectively combining the work of various disciplines on the team into a cohesive unit is one of the biggest challenges in wealth management.

When advice from different disciplines isn’t fully integrated, a plan to achieve a family’s multiple (and often conflicting) goals can fall short. Fortunately, ultra-wealthy families can take important steps to achieve best-in-class integration and maximize the value of their advisors’ work.

By leveraging an integrated wealth strategy, ultra-wealthy families have a much greater chance of meeting their needs and achieving their goals. But because implementing such a strategy can be difficult, advisors must pay heed to factors that may prevent its effectiveness and guide clients in the best way to achieve integration.

The wealth management ecosystem

For UHNW families, comprehensive wealth management extends beyond

investments, taxes, wills and trusts; it includes family

governance, leadership development, succession planning,

philanthropy and a host of other considerations. A thought

leadership model for organizing these needs and service areas –

The Ten Domains of Family Wealth (See Figure 1.) – outlines

various factors families should consider and provides a roadmap

for them and advisors to provide integrated, collaborative,

client-centered services for their benefit.

Figure 1: The Ten Domains of Family Wealth

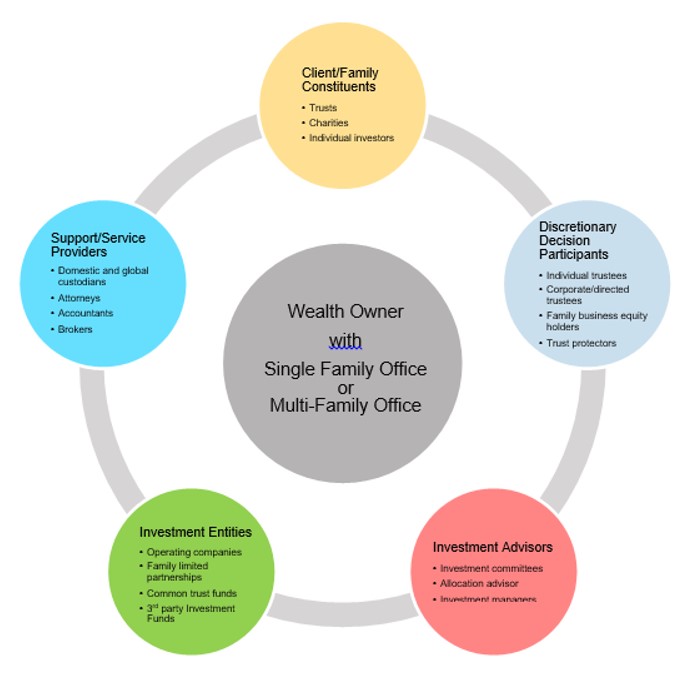

As a result of these factors, the wealth management ecosystem is

inherently composed of a large number of advisors and

constituents. (See Figure 2.)

Figure 2: The Wealth Management Ecosystem

The role of Integration in wealth management

Families with successful wealth strategies share a common view:

they acknowledge that integration adds value and find its

incremental costs to be worthwhile. These families recognize the

importance of two key factors.

The first is understanding and managing interdependencies. Effective wealth management is greater than the sum of its parts. All the elements need to work together toward a common purpose. A strategy has the best chance of succeeding when it is managed like a business, with a leader who ensures clear accountability and coordination across all functions. Every UHNW family that has run a successful business understands the importance of coordinating the work of various teams – human resource management, finance, sales and marketing – when making critical decisions and plans. Ultra-wealthy families benefit from applying many of the same governance and management practices to the management of their wealth.

The second key factor is seamless execution. A well-designed wealth strategy requires thorough, comprehensive planning. However, no strategy can be counted on to achieve important goals without timely and effective execution, which requires ongoing oversight, adaptation as circumstances change, and full integration of the work of professional team members and constituents.

Challenges to effective integration

If everyone agrees that integration is critical, why is it so

difficult to achieve? There are a number of obstacles that, for

simplicity, we sort into two major categories – weak client

commitment and poor team dynamics.

Hesitation is one example of weak client commitment. Effective integration requires dedicated and competent leadership. In some situations, neither the client nor any member of the client’s team wants to take a leadership role. This is often the case when the value of integration is under appreciated. Procrastination is another example of low commitment. Even when a wealth management leader is identified, that leader – a family member or one of the advisors – can delay accepting the role or responsibilities because of lack of confidence, competence or conviction.

Another factor contributing to low commitment is cost. The costs of integration present a dual problem. While we see an increasing demand from clients for integrated, objective advice, families are often reluctant to devote time to integration because they are apprehensive about the high cost of assembling numerous professionals, many of whom bill by the hour. From an advisor’s perspective, effective integration has proven expensive to deliver, given some combination of the need to either hire numerous professionals to provide different services and the need to oversee work delegated to other third parties. This demand-vs-supply imbalance presents challenges for clients and the wealth management industry to successfully develop and implement comprehensive plans.

Poor team dynamics represents the other major category of obstacles to effective integration. It is often evidenced by weak coordination, a narrow focus and conflict avoidance among team members. For example, the work of advisors chosen by the client may not be synchronized with other team members. The resulting weak coordination can complicate working relationships and a lack of trust among parties.

Also, advisors can be focused on their own area of expertise and not consider the overarching objectives of the family and the interdependencies with other disciplines. Such a narrow focus can lead to missed planning opportunities, administrative errors such as missed, erroneous or late filings. When attempting to achieve amicable working relationships, advisors may be concerned about being liked and accepted by others and avoiding conflict. As a result, they may not be effective advocates for solutions they recommend that may be unpopular but in the family’s best interest.

Additionally, competition, outdated skills, and conflicting egos are other common contributors to poor team dynamics. Advisors may view themselves as competing with each other for favored status with the family and a limited pool of fee income. In terms of skills, the expertise of some long-serving advisors may not be keeping pace with the changing wealth management landscape and increasingly complex needs of an ultra-wealthy family. Ungoverned egos can hinder effective teamwork, especially if team members believe their territories are being encroached upon.

Costs of poor integration

When wealth teams operate as a loose confederation of advisors

rather than as a cohesive unit, the client family may not achieve

critical strategic and financial goals. There are three main

reasons for this.

The first reason is poor performance and missed opportunities. Suboptimal transaction planning, e.g., for the sale of a business or real estate, can result in a failure to optimize the full value of important family assets. And attractive opportunities to grow or protect assets can fall through the cracks if team members do not collaborate.

The second reason is higher costs. Ineffective integration and planning can lead to the overpayment of taxes. For example, poor asset location decisions about allocating assets among taxable, tax-deferred and tax-exempt accounts can lower the tax efficiency of a family’s total portfolio. Missed opportunities to take advantage of tax-loss harvesting can also increase a family’s tax bill. Finally, families may incur higher costs if the work done by various team members is not monitored closely or is liable of being duplicated.

The third reason is incomplete plan execution. Every wealth

management strategy, no matter how well conceived or mapped out,

will encounter barriers to execution or implementation. Those

barriers may be in the form of poor communication between members

of the clients’ team of advisors, a lack of clarity about

responsibilities, or failure to anticipate and understand where

gaps exists in the strategy. The result is that only a portion of

a client’s plan or strategy will be successfully implemented

rather than 100 per cent of it, obviously a suboptimal

outcome.

How to achieve integrated wealth management

Accomplishing complete integration is challenging, to be sure.

But by taking certain actions, wealth owners can ensure that

their strategies are being managed in a unified manner. These

actions include achieving clear accountability and outstanding

communication, ensuring advisors have the right skills and

competencies, aligning compensation, and using technology

effectively.

Clear accountability

There are three ways to achieve clear accountability. The first

is to identify a leader accountable for assembling and overseeing

the work of team members. Define the exact duties, expectations

and scope of authority of that position. The second way is to

ensure that the leader selected has the requisite skills,

relationship capital and support of the family to succeed. The

third way is to specify the roles, responsibilities and

expectations of family members, family office executives,

non-family professionals and other stakeholders who will

collaborate with the leader to implement strategies.

Outstanding communication

Outstanding communication can be achieved in four ways. First,

articulate the family’s values, strategic goals and mission, then

ensure that each member of the family’s wealth ecosystem

understands them. Second, maintain an effective planning

schedule, conduct frequent meetings with the team and create

detailed minutes that document the decisions made, issues to be

addressed and actions to be taken.

Make sure responsibilities for tasks, expected deliverables and timetables are clear. Third, manage a disciplined process that ensures execution and follow-up. Fourth, include external advisors in all relevant communication.

Skills and competencies

Ensuring that advisors have the right skills and competencies can

be accomplished in two ways. The first is to select a team of

high-quality professionals with experience of being effective at

the UHNW level. As a colleague once described, a high-performing

team should consist of problem solvers who not only have the

ability to “see the bus coming” but the ability to “stop the bus”

if needed. The second is to build a network of professionals

across the full range of areas in family wealth, e.g.,

investments, tax, estate planning, governance, leadership, family

development, health and wellness, and philanthropy. The family

should have access to experts in all 10 domains within the team

or by qualified referrals.

Alignment of compensation

To align compensation, ensure that advisor and employee

compensation are free of conflicts of interest or hidden biases

toward products or services.

Technology and reporting

To make sure that you are using technology effectively, start by

incorporating platforms that are able to generate reports

connecting information and accounts to provide a holistic view of

family wealth, not just isolated investments. Also, use

technology that enables information sharing among advisors and

implement email aliases, encryption and other cyber practices to

enhance security and simplify communication with team members.

Other examples include applying client relationship management

(CRM) technology to manage workflow and using digital tools,

including mobile technology, to strengthen 24/7 access to

information.

While an integrated wealth strategy takes time and effort to develop, the payoff is well worth it. With comprehensive planning and oversight, UHNW families have a much greater chance of achieving critical family goals and meeting the needs of the current and subsequent generations.