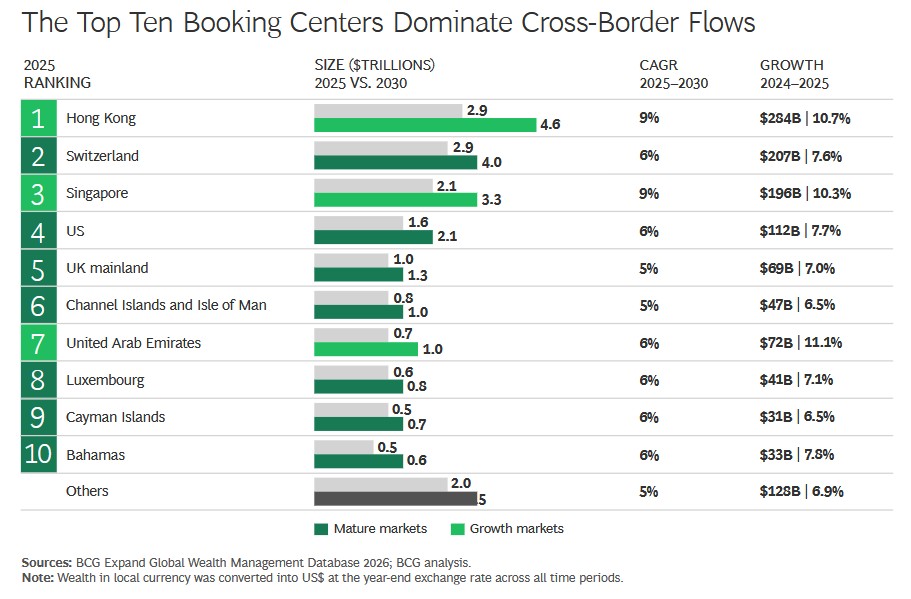

In the rankings of cross-border financial centers, the US is not the largest but has a still-significant total of $1.6 trillion of such wealth as of last year, and will rise to $2.1 trillion by the end of this decade, a report says today.

The US is the fourth-largest such center, Boston Consulting Group said in its Global Wealth Report 2026.

Hong Kong has now matched Switzerland as the world’s largest cross-border wealth hub – host to $2.9 trillion of such flows – and is slated to overtake the Alpine state, rising to $4.6 trillion at the end of the decade. The report noted that the top international financial centers increasingly dominate the cross-border space.

Switzerland, which for decades has been the top cross-border jurisdiction, will reach a still-impressive $4 trillion by 2030. Singapore reached $2.1 trillion at the end of 2025 and is expected to expand to $3.3 trillion. The US stands at $1.6 trillion and will rise to $2.1 trillion .

For some time, BCG and other organizations have predicted that Hong Kong, benefiting from closer integration with mainland China – and helped by a vibrant IPO market and the Wealth Connect system – would eventually claim the top spot.

The UK mainland has total cross-border wealth of $1 trillion and is expected to host $1.3 trillion by 2030. During the time the BCG report covers, there has been political and media controversy about the UK’s decision to axe its resident non-domicile regime and move to a system containing a four-year pause on foreign income and gains taxes.

In total, cross-border wealth rose 8.4 per cent to $15.7 trillion in 2025, lifted by market performance and HNW individuals spreading risks around the world. The top 10 booking centers took almost 90 per cent of new cross-border flows. They also hold over 80 per cent of existing stock. Concentration is not new in this industry, but it is intensifying.

Turning to Singapore, BCG said the city-state is “positioned as the most diversified wealth hub in Asia, serving as a neutral conduit between Asian and Western capital markets. That role has made it a beneficiary of safe-haven flows amid US-China tensions.”

Regulatory stability, institutional credibility, and a strong wealth management ecosystem have attracted more than 2,000 single family offices to Singapore and more than 100 independent wealth management firms, the report said.

Under the report strapline of “The Great Reordering,” BCG said total global financial wealth rose 10.7 per cent from a year ago to $333 trillion in 2025, despite a backdrop of trade wars, tariff arguments and escalating geopolitical tension. From 2025 to 2030, BCG predicts a compound annual growth rate of 7 per cent.

Including real assets such as property, net wealth reached $550 trillion, up 9.3 per cent. The gains were not evenly distributed. Equities surged by 13.2 per cent while real assets expanded by 7.4 per cent. Gold was the standout, rising by about 44 per cent, supported by retail buyers and central bank acquisitions amid worries about currency volatility.

Asia-Pacific

The Asia-Pacific region remained a major growth engine, supported by its central role in the AI supply chain, from semiconductor exports in South Korea to accelerating data center investment across Southeast Asia, and strong equity market performance in Hong Kong and Japan. Mainland China led the region, with financial wealth expanding by 15 per cent in 2025 and projected to grow at 9 per cent annually through 2030. The rest of Asia-Pacific grew by 9.2 per cent, with 7 per cent annual growth expected over the same period.

Western Europe

BCG said Western Europe sprung a positive surprise, rising 15.3 per cent. This growth was supported by favorable currency movements and a persistently high household savings rate.

That said, BCG noted that the region’s underlying equity market performance remained modest, driven by weaker economic momentum and limited exposure to high-growth sectors. Over the next five years, wealth creation in the region is expected to grow at an annual rate of 5 per cent.

MENA region

In the Middle East and Africa, nominal wealth grew 12.3 per cent in line with a broader rally in emerging markets. Accelerating economic diversification and strong investment activity in the Gulf States underpinned this growth, alongside robust gross domestic product expansion across Sub-Saharan Africa.

North America

North America’s wealth grew 7.4 per cent, decelerating from the fast pace of an “exceptional” 2024. A weaker US dollar offset strong equity gains, while performance remained concentrated in a narrow group of mega-cap technology stocks.

“That concentration leaves the market vulnerable to a correction if the AI capital expenditure cycle turns,” BCG said.

North American growth is expected to average around 7 per cent annually through 2030, in line with global wealth.

Future wealth drivers

Looking ahead, the report said emerging markets will add $12 trillion of financial wealth and account for roughly 10 per cent of global wealth growth between now and the end of the decade. The affluent-and-above segment – individuals with more than $250,000 in financial wealth – is forecast to grow at an average of 8 per cent annually in these markets through 2030, adding over one million dollar millionaires by 2030.

India will add more than $2 trillion in total wealth by 2030, followed by Brazil at $1 trillion and Mexico at $600 billion.

Under a title of “the segment that nobody is serving,” BCG said the “most attractive segment for wealth managers is the affluent and emerging high net worth tier, broadly defined as clients with $250,000 to $5 million in investible assets.

“In emerging markets, this group is large, growing fast, and structurally underserved. They have outgrown standard deposit products, particularly as interest rates fall, but do not yet qualify for the full-service models that international wealth managers reserve for larger clients. And the international players in many emerging markets are pulling back.

“Rising compliance costs, tighter cross-border requirements, and a broader push to reduce complexity have led global wealth managers to concentrate on clients with $5 million and above, leaving the affluent and lower HNW segment increasingly to local players,” it said.

On other topics, the report touched on AI, concluding that the technology is more likely to disrupt rather than replace human advice.

“Firms that layer AI tactically on existing processes will see moderate near-term benefits. But the biggest payoff will go to true AI-first organizations, those that redesign workflows and processes around AI agents end to end. That effort takes more upfront investment, but these firms will capture impressive efficiency gains and outpace peers with lower pricing, greater profitability, and a richer, more customizable product and service portfolio,” it said.