Whatever the wisdom of enabling holders of 401 retirement accounts to hold private market assets such as private credit, “democratization” of such alternative investments is the new reality. It is an investment “vibe shift.”

With more firms staying private, or taking longer to enter a stock market, there is a public policy concern over whether the broad public are being frozen out of sources of return if they are barred from holding private market assets . On the flipside, there are risks to this step, and we have heard skeptical comments about how wide access to private markets should be. A recent round of redemptions from some private credit funds, with retail investors in the mix, have raised fresh worries.

PricewaterhouseCoopers estimates that even a 5 per cent allocation to alternatives across 401s could unlock more than $1 trillion in new assets by 2030, or roughly $7 billion to $19 billion in annual industry revenue. Given wealth management’s focus on margins and revenues, it is easy to see the dynamics in play.

How quickly the move toward holding private market investments into 401s and equivalent vehicles outside the US will go depends on meeting strict consultant and fiduciary standards, particularly around valuation governance, liquidity design, operational readiness and fee transparency.

PwC’s asset and wealth management leader, Roland Kastoun, has a ringside seat on what the wider wealth sector thinks of the “democratization” move. Moonfare, the Germany-headquartered digital private asset platform, also brings its own angle. Both firms recently spoke to this publication about developments.

"On balance, this is a net positive for the industry. The scale of the opportunity is significant. Even a modest allocation to alternatives across 401 plans could unlock substantial new assets and revenue for the sector,” Kastoun said. “This isn't a zero-sum game with existing products; it's additive. It creates a new distribution channel for alternative managers and adds a differentiated return stream for participants.

“That said, it will take deliberate planning and significant effort to make it work. The operational complexity is real: daily participant-level accounting, liquidity management, valuation governance, fee transparency, and other requirements all represent high bars that many managers are not yet equipped to meet. The problems are solvable, but they require sustained investment and cross-ecosystem coordination. Rushing into 401s without the infrastructure and proper guardrails risk reputational and fiduciary exposure,” Kastoun said.

Getting the details right will be critical, which is why the sector should not rush in.

Handling the valuations of such retirement accounts is challenging, given that private market investments’ net asset values for example tend to follow a quarterly rhythm, rather than something more frequent, Kastoun said.

“These funds need to manage cash coming in on a regular basis, such as amounts withheld from monthly or biweekly pay, which could be `waiting’ until it is deployed when attractive opportunities are available. This can lead to a significant drag on returns,” he explained. “On the positive side, because 401 plans are designed to be held for decades, their time-horizons should fit well with the typical liquidity and characteristics of private markets. One challenge persists however, addressing the portability/liquidity question when people change jobs or want to roll over retirement savings.”

There are upsides to consider.

“In theory, 401s should work better for private markets because you can do asset-liability matching in a more predictable way,” Kastoun said.

What’s happening to make this a reality?

"We're seeing several categories of solutions emerging. First, the large recordkeepers and target-date fund providers are working to adapt their infrastructure to accommodate semi-liquid private market assets. That includes upgrading data feeds, updating modeling and cashflow forecasting capabilities, enhancing valuation processes, and improving participant-level accounting to handle what is a fundamentally different operational cadence,” Kastoun said.

“Second, there's a growing ecosystem of providers building the connective tissue between alternative asset managers and DC platforms. Think valuation service providers, liquidity management tools and data standardization layers. Third, some alternative managers are redesigning their products for defined contribution compatibility, including building additional valuation capabilities to provide daily NAVs for existing products,” he said.

A test

The recent private credit strains have been an important test.

Philip Meschke, private equity investments head at Moonfare, said what happened represents a maturation of the sector, not a setback.

“The 'easy phase' of private credit is over. Established managers have built out their origination networks, investment pipelines and sector expertise. Meanwhile newer entrants are operating in a more competitive market and, in some cases, taking risks in areas where they may have less experience. While the overall asset class still has solid fundamentals, the dispersion between strong managers and the rest is likely to become more visible,” Meschke said.

“There are also important regional and sector distinctions. In the US, private credit has expanded rapidly into a much wider range of sub-industries, and that is where some of the more concerning pockets of bad lending appear to sit. Europe still looks closer to the more traditional private credit model, where private credit funds have replaced some lending activity historically undertaken by banks. The latter remains the area we would generally view as better insulated,” he continued.

“Crucially, the usual crisis signals are not flashing red. Credit spreads in parts of the high-yield and loan markets are not especially elevated, there is limited stress in the banking system, growth remains relatively robust and interest rates, while higher than in the previous cycle, are not pointing to a systemic break. Defaults and overdue loans may rise, and investors should watch the credit cycle carefully, but today’s weakness looks more like pockets of stress than a market-wide collapse,” he said.

PwC’s Kastoun thinks useful lessons have hopefully been learned.

"The recent stress in corners of the private credit market has been a useful reminder that growth and risk management must advance in tandem. Private credit has been on an exceptional growth trajectory in both size and breadth, and during that growth phase, sponsors have been on a steady journey toward further institutionalization,” Kastoun said. “Current events, while idiosyncratic and confined to specific segments, are raising legitimate questions about underwriting quality, valuation trust, governance, and the interconnectedness of participants across the ecosystem,” he said.

“We don't view this as a decisive event that derails the asset class. Investors are not abandoning private credit. Institutional investors for instance are focused on working with managers who are best equipped to handle volatility, have the best access to high-quality origination, and are able to deliver at scale with strong underwriting discipline and transparency,” he said.

“For the 401 conversation specifically, this is instructive. It reinforces why consultants and fiduciaries are right to demand rigorous standards around valuation governance, liquidity design, and operational readiness before these assets enter retirement plans. The bar should be high, and recent events validate that approach,” Kastoun said.

Margins

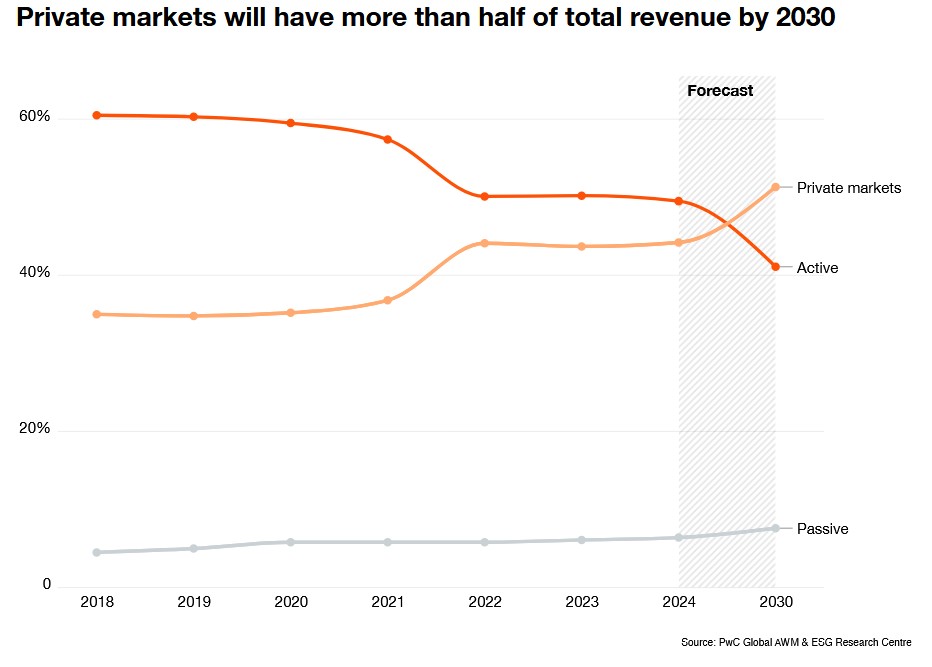

The move for wider access – including the adjustment to the SEC’s Accredited Investor Rule – comes at a time when wealth and asset management margins are under pressure from forces including AI and commodization of parts of the sector value chain. The enthusiasm for private markets speaks to a desire for more diverse – and hopefully higher-margin, revenue streams. Last year, PwC said private markets are set to “remain the industry’s most profitable engine.” Private markets generate roughly four times more profit per billion dollars of AuM than traditional managers today. By 2030, private markets revenues are set to reach $432.2 billion and deliver over half of the total asset management industry’s revenues by 2030.

Private markets generate roughly four times more profit per billion dollars of AuM than traditional managers today. By 2030, private markets revenues are set to reach $432.2 billion and deliver over half of the total asset management industry’s revenues by 2030.

“The margin story here is more nuanced than it might appear at first glance, because it plays out very differently depending on where you sit in the value chain,” Kastoun said.

“For the firms that provide the wrappers, such as target-date fund managers, managed account providers, and the services providers in the ecosystem, this is a relatively straightforward margin opportunity. They can point to a differentiated return stream embedded in their default product and justify a modestly higher fee than a purely passive allocation would command. Their infrastructure will need to be upgraded but they're adding a sleeve, not building a new business,” he said.

“For the private market managers themselves, the large alternative asset managers who would provide the underlying building blocks, the economics are more complex. To access the defined contribution channel, they will need to build a robust operational ecosystem, including participant-level reporting, daily or near-daily valuation capabilities, liquidity management frameworks, data standardization across recordkeepers and custodians, and fiduciary-grade transparency. That's a significant investment.

“They'll also likely need to offer these building blocks at fee levels below what they currently charge high net worth or retail clients because the DC system is structurally a low-margin, high-scrutiny environment where fee justification is intense and competitive,” he said.

Not a stampede

Kastoun does not expect a rush by retirement funds into alternatives.

"The pace will be measured, not explosive, at least initially. Consultant comfort is the binding constraint on adoption, and consultants will move deliberately. They'll want to see track records of these structures operating within DC plans without incident before broadly recommending them,” he said. “That said, we've seen how quickly the DC system can adopt new defaults once they're established. Target-date funds went from a niche product to the practical default option for 401 contributions in a relatively short period. The same acceleration could happen here once the early movers prove the model works.”

Moonfare’s Meschke had further thoughts about the recent private credit problems.

“This period has reiterated how liquidity in private markets is conditional, not guaranteed. 'Semi-liquid’ or ‘evergreen’ products aren’t the same as daily dealing public-market funds. They may offer periodic access to capital, but that access comes with trade-offs.

“Managers may need to hold more cash or liquid assets, pace deployment more carefully and manage redemptions through caps, fees or gates. Those features are not necessarily flaws and can act as a circuit breaker in moments of stress, helping to protect investors against forced selling of illiquid assets at poor prices. The most credible managers will set these expectations early and clearly.

“Private credit, leveraged loans and syndicated loans all sit within the broader 'credit’ universe, but they differ in structure, liquidity, origination and investor protections. Private investors may understand the headline appeal of private credit – income, diversification and access to non-bank lending – without always appreciating the differences between a directly originated, illiquid loan and more tradable forms of credit exposure,” he added.