Investment Strategies

Investors Put Chips Back On The Table, But Worries Linger â State Street

Equity exposure and sentiment has gyrated since the November elections. Recent measures of worry suggest that confidence is improving. The State Street indices of sentiment measure what investors are actually doing.

The US administrationâs delay in imposing the sweeping âLiberation Dayâ tariffs has emboldened investors to put chips back on the table in equity markets. A State Street risk barometer suggests that appetite for equities rose in May.

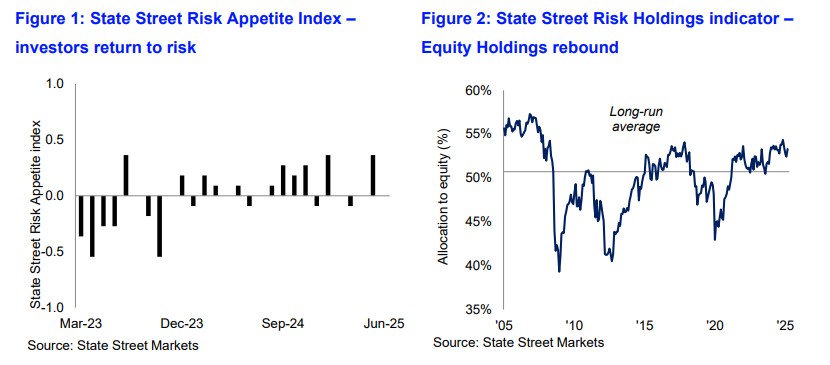

The State Street Risk Appetite Index rose to 0.36 at end-May. The State Street Holdings indicators show that long-term investor allocations to equities rose anew in May to levels last seen just before the April 2 tariff announcement.

During May, exposure to equities rose by 0.9 per cent relative to a 0.8 per cent fall in bond holdings.

Equity exposure has whipsawed since Donald J Trump was elected President last November. Initially, stocks rose, then fell â particularly among tech stocks â after revelations about Chinaâs DeepSeek AI app â and fell dramatically after the tariff announcement. Theyâve subsequently made up ground, although sentiment remains relatively skittish.

âFear gaugesâ such as the VIX Index, which measures options volatility on the US S&P 500 Index of major stocks, started at 17.93 per cent on January 2, 2025, rose to almost 28 at one point in March, and skyrocketed to 52.33 on April 8 after the tariff announcement. Since then, the VIX has gradually fallen, and was last seen around 17.57 today.

âWhile the narrative around trade tariffs remains ubiquitous, implementation delays allied to lower effective tariff rates than initially envisaged helped lift sentiment towards risk as did the (still) largely benign environment for inflation that undermines fears around stagflation,â Dwyfor Evans, head of APAC macro strategy, State Street Markets, said.

âProtectionism and trade tariffs likely exert a greater impact on mercantilist Asia than anywhere in the global economy, particularly given the regional build-up of (predominantly) dollar reserves. A weaker dollar and higher US yields thus matter, as do tariffs,â he said.

The State Street risk indicator measures investor confidence or risk appetite quantitatively by analyzing the actual buying and selling patterns of institutional investors derived from State Streetâs $44 trillion in assets under custody and administration.

The Risk Appetite Index is derived from measuring investor flows in twenty-two different dimensions of risk across equities, foreign exchange, fixed income, commodity-linked assets, and asset allocation trends. The index captures the proportion of the 22 risk elements that saw either risk seeking or risk reducing behavior. A positive reading suggests that on balance investors are adding to their risk exposures, while a negative reading suggests risk reduction. State Streetâs holdings indicators capture the share of investor portfolios allocated toward equity, fixed income and cash going back to 1998.

ETFs

There are other indications that sentiment about equities â and

US equities in particular â has recovered to some degree.

Although inflows in exchanged-traded funds in May were still well

below the 12-month average, they were positive for the first time

on a three-month view. ETFs focused on Europe saw

weaker growth than recently (source: etfbook.com, as of May

30).

"Relaxing signals in the trade dispute between China and the USA impacted the ETF market in May. Investors turned more towards the USA again," Stefan Kuhn, head of ETF distribution for Europe at Fidelity International, said.

"It is quite conceivable that Trump's renewed tariff threats against the EU are already affecting net inflows into European equity ETFs," he said. Additionally, the markets in Europe have performed very well this year, Kuhn said: "Investors are asking themselves how much upside potential European stocks still have."

Overall, the ETF market grew by $30 billion in May, stronger than in April.