Family Office

Drivers Of Family Offices' Wealth Evolve; Investments Shift To Europe, Asia â Data

An annual barometer of the scale and scope of the world's family offices sector shows that the liquidity events that mint new FOs are changing, with slightly less coming in 2025 from the real estate area. There has also been a reallocation of investment toward Europe and Asia.

An annual report on the makeup of family offices from FINTRX, a private wealth intelligence platform, shows that their prime sources of liquidity shifted somewhat during last year. It has also noticed an investment shift to Europe and Asia in 2025.

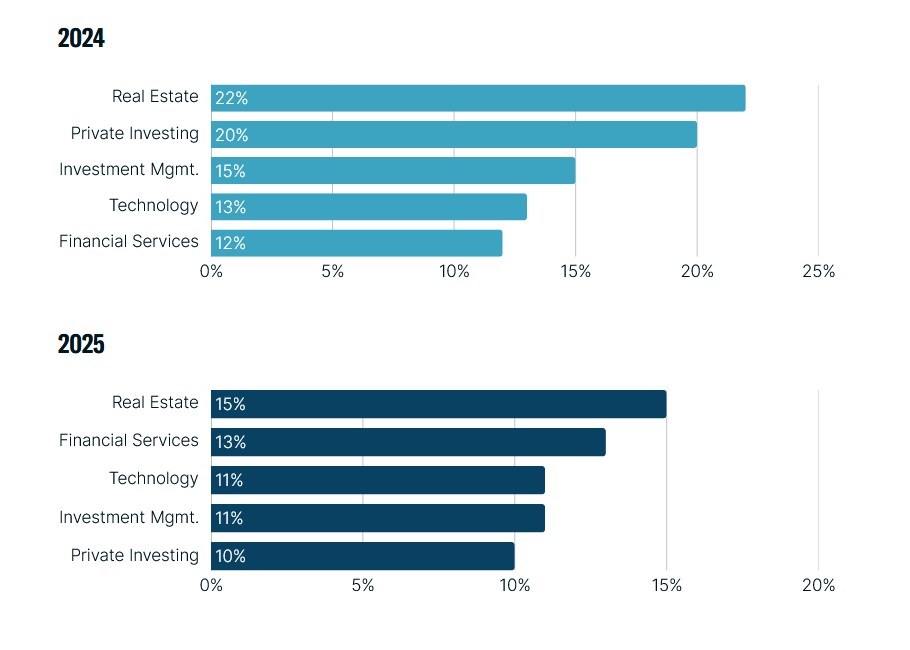

In 2024, sources of wealth were concentrated in real estate and private investing, with investment management, technology, and financial services also representing meaningful shares. In 2025, however, that concentration moderated. Real estate accounted for a smaller share, while financial services increased modestly, and other categories represented a more evenly distributed mix across wealth origins, the firm said in its Family Office Industry Report.

âExposure across industries is broadening: As transaction volume increased, concentration in a small number of areas declined. Family offices are allocating capital across a wider set of industries beyond their historic tilt toward finance and real estate, with growing interest in areas such as technology, healthcare, and specialized real estate themes,â it said. (See chart below.)

Source: FINTRX 2025 Family Office Industry Report

FINTRX said direct investment activity remains âstrong.â Among family office firms added to its database, the group said it tracked more than 1,500 direct investments in private companies and more than 150 real estate deals.

Such data reports come at a time when the scale and reach of family offices, once an obscure area with limited media coverage, continue to increase. According to Deloitte, there were about 8,000 family offices in 2024 and it predicted that number would surpass 10,720 by 2030 on current trends.

Another trend from the report, FINTRX said, is geographic rebalancing toward Europe and Asia. These regions accounted for a larger share of net new family offices than in prior years. Rising activity in these regions and an expanded research footprint in historically âunderrepresented marketsâ are both contributing factors, it said.

In another geographic point, North America remained the largest region represented among net new family offices added to the FINTRX dataset, though its share declined from about 68 per cent in 2024 to 49 per cent last year. Over the same period, Europe increased from 16 per cent to 27 per cent, while Asia rose from 9 per cent to 13 per cent, reducing the regional concentration observed in the prior year.

FINTRX said that in net terms â taking account of departures â it added 442 net new family offices to its private wealth intelligence platform. This increased the size of its dataset by more than 10 per cent. Single-family offices continued to represent about two-thirds of family offices, while firms founded between 2010 and 2019 comprised the largest share of entrants across both periods.